J2: Exchange Rates

TYS 2023 Q4b

Discuss whether management of the exchange rate is the most appropriate way of controlling inflation in Singapore. [15]

Introduction:

Inflation refers to the sustained increase in the general price level over time. As a small, open economy, Singapore is highly vulnerable to imported inflation, given its reliance on imported food, energy, and raw materials. To control inflation, the Monetary Authority of Singapore (MAS) primarily manages the exchange rate (S$NEER) within a managed float system, rather than using interest rates like many other central banks.

Beyond imported inflation, Singapore is also prone to demand-pull inflation due to its position near full employment, with an unemployment rate of 1.9% in 2023, below the Non-Accelerating Inflation Rate of Unemployment (NAIRU). Tight labor market conditions can drive wage growth and domestic cost pressures, further fueling wage-push inflation. This essay will discuss the effectiveness of exchange rate management in controlling inflation in Singapore while considering alternative policy measures.

R1: Exchange Rate Management as the Most Appropriate Tool to Control Inflation

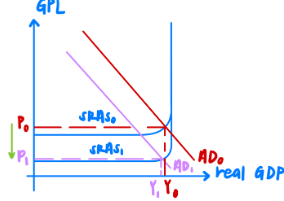

Exchange rate management is a key pillar of Singapore’s inflation control strategy, overseen by the Monetary Authority of Singapore (MAS). By appreciating the Singapore dollar (SGD), the price of Singapore’s exports will be more expensive in foreign currency while imports will be seen relatively cheaper in domestic currency. Assuming that Marshall Lerner’s Condition holds (PEDx + PEDm > 1), there will be a more than proportionate fall in demand for Singapore’s exports. Additionally, there will be a more than proportionate increase in demand for imported goods as locals will switch over to consume the relatively cheaper imported products. This will lead to an increase in short-run aggregate-supply (SRAS) from SRAS0 to SRAS as the reduction in prices of imports leads to lower cost of production. General price level falls from P0 to P1, thereby alleviating cot-push inflation.

Furthermore, as export earning decreases as the price of Singapore’s exports is more expensive in the foreign market, while import expenditure increases, net exports will fall, leading to a fall in AD from AD0 to AD1. This reduces the upward pressure on price thus curbing demand-pull inflation as well.

EV1: Evaluation of Exchange Rate Management as the Most Appropriate Tool

While exchange rate management is effective in controlling inflation, it can lead to unintended consequences, such as a reduction in real national output (NY) and economic growth. An appreciation of the Singapore dollar (SGD) increases the price of exports in foreign currency (Px↑) and decreases the price of imports in domestic currency (Pm↓), leading to a fall in net exports (X - M). Since net exports are a component of aggregate demand (AD), a decline in (X - M) results in a fall in AD, causing lower NY and slower economic growth.

However, Singapore’s heavy reliance on imports for production inputs helps to offset some of these negative effects. Lower costs of imported raw materials, capital goods, and intermediate goods in domestic currency reduce firms’ cost of production (COP), allowing firms to pass on these cost savings in the form of lower prices, helping to maintain or even improve price competitiveness despite the appreciation. As a result, the decline in net exports may be less significant than initially expected, reducing the overall contractionary impact on AD and NY.

OR

However, Singapore’s key exports, such as electronics, refined petroleum products, and chemicals, often have inelastic global demand as they are essential components in various industries worldwide. Since these goods do not primarily compete on price but quality, an appreciation of the SGD is unlikely to significantly reduce demand for exports. This further mitigates the negative impact on AD and economic growth, making exchange rate management a viable tool for inflation control without severely harming external demand.

R2: The Need for Supply-Side Policies to Address Wage-Push Inflation

While exchange rate management is effective in controlling imported inflation, it does not directly address wage-push inflation, which occurs when wages rise faster than productivity, increasing firms’ cost of production (COP). Given Singapore’s tight labor market, with an unemployment rate of just 1.9% in 2023, below the NAIRU, labor shortages contribute to upward wage pressures, making it crucial to implement supply-side policies that increase labor supply and enhance productivity.

One such policy is raising the retirement age, which increases the quantity of labor available in the workforce. The Singaporean government has progressively raised the retirement age, with plans to increase it to 65 by 2030, ensuring that experienced workers remain in the labor force for a longer period. This expands the labor pool, reducing the pressure on firms to compete for workers by raising wages, thereby mitigating wage-push inflation. In addition to increasing labor supply, supply-side policies can also enhance the quality of labor by improving worker productivity. Initiatives such as SkillsFuture and the Productivity and Innovation Credit (PIC) scheme encourage firms to invest in worker training and adopt new technologies, helping workers upgrade their skills and become more efficient. A more skilled workforce allows firms to produce more output with the same level of input, reducing unit labor costs and increasing productive efficiency.

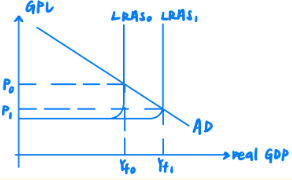

As a result, these supply-side measures shift the Long-Run Aggregate Supply (LRAS) curve rightward from LRAS0 to LRAS1, increasing the economy’s productive capacity from Yf0 to Yf1. General price level also falls from P0 to P1. By ensuring that inflationary pressures are controlled through higher labor supply and greater efficiency, these policies complement exchange rate management in achieving long-term price stability and sustainable economic growth.

EV2: Limitations of Supply-Side Policies in Addressing Wage-Push Inflation

While supply-side policies such as raising the retirement age and workforce upskilling can help increase the quantity and quality of labor, their impact on inflation is not immediate and may take years to show significant results. The effectiveness of these policies depends on how quickly older workers adapt to workforce demands and whether firms are willing to hire them. If firms prefer younger, more adaptable workers, the increase in labor supply may be slower than expected, reducing its effectiveness in controlling wage pressures.

Moreover, while productivity-enhancing policies such as SkillsFuture and automation incentives can improve long-term efficiency, they require significant investment and structural adjustments. Firms may hesitate to adopt new technologies or retrain workers due to high upfront costs and uncertainty about returns, delaying the intended benefits.

Conclusion:

In conclusion, whether exchange rate management policy is the most appropriate way to control inflation in Singapore depends on the root cause of the inflation. While exchange rate policy can effectively tackle both demand-pull inflation and imported inflation, it will lead to unintended consequences such as a fall in actual economic growth if the fall in AD outweighs the increase in SRAS. It also does not address wage-push inflation, thus the need for supply-side policies. However, supply-side policies are a long-drawn process and are subjected to the receptiveness of the workers. Since Singapore has a complex inflationary landscape due to its susceptibility to imported inflation as well as demand-pull inflation as it is operating near the full employment output, a mic of policies should be used. Exchange rate policy can be used in the short term to address demand-pull and imported inflation to ease the over-heated economy. Whereas supply-side policies can be implemented in the long-run to increase the productive capacity of the economy to reduce the vulnerability of Singapore’s economy to both demand-pull and cost-push inflation.