J2: Exchange Rate Systems (Appreciation)

SAJC 2022 Q5

(a) Explain why Singapore chooses to tighten its monetary policy by appreciating its currency rather than by raising interest rates. [10]

Introduction

Monetary policy refers to the use of interest rates or the exchange rate to influence inflation and economic activity. While most large economies raise interest rates to manage inflation, Singapore chooses to tighten monetary policy by appreciating the Singapore dollar (SGD). This is due to the cost-push nature of Singapore’s inflation, the constraints of the macroeconomic trilemma, and the structure of its small and open economy.

R1: Singapore does not use interest rates because inflation is largely cost-push

In countries such as the US or UK, inflation is typically demand-pull in nature. Central banks raise interest rates to reduce consumption (C) and investment (I). A higher interest rate increases the cost of borrowing (COB), discouraging households from purchasing big-ticket items like cars and property, while firms delay capital expenditure due to higher financing costs. As both C and I fall, Aggregate Demand (AD) falls from AD₀ to AD₁. Through the reverse multiplier effect, the general price level (GPL) falls from P₀ to P₂, curbing demand pull inflation.

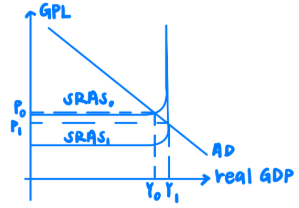

However, Singapore’s inflation is mainly cost-push due to its high dependence on imports for food, energy, and intermediate goods. With imports exceeding 130% of GDP and a trade-to-GDP ratio above 300%, Singapore is highly exposed to global price shocks. Since inflation is driven by rising costs, not overheating demand, raising interest rates would have limited impact. Instead, MAS appreciates the SGD to lower imported input prices (Pm), reducing unit costs of production. This shifts SRAS rightward from SRAS₀ to SRAS₁, causing a fall in GPL from P₀ to P₁.

R2: Interest rate policy is not feasible due to the macroeconomic trilemma

Singapore also does not use interest rate policy because of the macroeconomic trilemma. As a global financial hub, Singapore allows free capital mobility to attract investment and maintain financial credibility. At the same time, MAS manages the exchange rate through the S$NEER basket to ensure price stability. Under the trilemma, a country cannot simultaneously maintain a managed exchange rate, free capital flows, and an independent interest rate policy. Singapore sacrifices interest rate autonomy to retain the other two.

If MAS were to raise domestic interest rates, Singapore’s rates would become relatively more attractive than those of other countries, leading to capital inflows (hot money). This increases demand for the SGD, causing it to appreciate sharply. The resultant exchange rate volatility is undesirable for a trade-dependent economy like Singapore, as it affects export competitiveness and makes import prices unpredictable, creating inflation instability. As such, Singapore is effectively an interest rate taker, with domestic rates influenced by global conditions rather than local policy.

R3: Singapore’s small and open economy makes exchange rate policy more effective

Even if Singapore faces demand-pull inflation, exchange rate policy remains more effective than interest rate policy due to the structure of its economy. Singapore has a small domestic market, with a limited consumer base and heavy reliance on net exports (X–M) and foreign demand as the main drivers of growth. As such, interest rate policy—which primarily works through changes in consumption (C) and investment (I)—has limited traction.

Instead, MAS can use exchange rate appreciation to influence AD directly through the external sector. An appreciation of the SGD makes exports more expensive in foreign currency terms (Px↑) and imports cheaper domestically (Pm↓). Assuming Singapore’s exports are price elastic, this leads to a more than proportionate fall in export revenue and a rise in import expenditure. As net exports fall, AD falls from AD₀ to AD₁, and the general price level (GPL) falls from P₀ to P₁. This helps to ease inflationary pressures and prevent overheating, especially since Singapore often operates close to full employment Yf given it s unemployment rate is 1.9%, below the natural rate of unemployment.

Conclusion

In summary, Singapore chooses to tighten monetary policy through exchange rate appreciation rather than interest rate hikes due to the cost-push nature of its inflation, the infeasibility of interest rate autonomy under the trilemma, and the limited effectiveness of interest rate policy in a small and open economy. Exchange rate policy allows MAS to manage inflation more directly and with greater precision, while preserving external stability and supporting Singapore’s export-oriented growth model.