J2:Monetary Policy (Pt2)

NYJC Q3b

The Monetary Authority of Singapore (MAS) has a unique monetary policy framework that focuses on managing the exchange rate rather than interest rates. This approach has implications for the country's macroeconomic objectives.

(b) Assess whether the use of monetary policy to achieve low inflation will lead to trade-offs in the Singapore economy.

Introduction

There are two types of inflation, demand-pull inflation and cost-push inflation. Demand pull inflation refers to a sustained increase in general price level due to an excessive rise in aggregate demand (AD) with constraints in aggregate supply (AS). Cost-push inflation consists of imported inflation and wage-push inflation, it refers to the rise in general price level due to an increase in cost of production. Whether the use of monetary policy to achieve low inflation will lead to trade offs will be further discussed below.

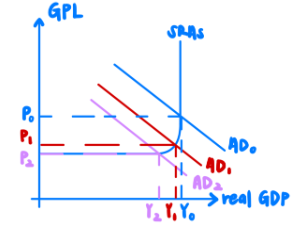

R1: Explain why appreciation will curb demand-pull inflation but will lead to a fall in economic growth

Appreciation can be used to curb demand-pull inflation. When the Singapore government adopts appreciation, the Singapore Dollar (SGD) will be strengthened. With a stronger SGD, Singapore’s domestically produced goods will become more expensive in foreign currency while imports will become cheaper in domestic currency. When the prices of Singapore’s exports increase, it will lead to a more than proportionate fall in quantity demanded of exports, assuming that the demand for Singapore’s exports is price elastic. This will lead to a fall in export earnings (X). At the same time, imported goods will be seen as relatively cheaper as compared to domestic goods. A decrease in prices of imports will lead to a more than proportionate increase in quantity demanded for imports, assuming that the demand for imports is price elastic. This will subsequently lead to an increase in import expenditure (M). A fall in X and a rise in M will cause net exports (X-M) to fall, thus leading to a decrease in AD from AD0 to AD1. This will trigger the reverse multiplier process whereby several rounds of spending and re-spending are lost, leading to a multiplied fall in national income. The general price level falls from P0 to P2 and AD will eventually decrease from AD0 to AD2 and national income falls from Y0 to Y2, resulting in falling economic growth. As national income falls, output decreases and there is an unplanned inventory accumulation, thus decreasing the derived demand for labour, causing the unemployment rate to increase.

Evaluation 1: Size of multiplier, PED of exports & state of economy

However, Singapore's key exports such as pharmaceutical products, petroleum, and chemical products are price inelastic. Thus, an increase in prices of exports due to a stronger SGD will only lead to a less than proportionate fall in quantity demanded for Singapore’s exports. This indicates that Singapore will still be able to maintain its export earnings, only experiencing a slight decrease. Additionally, Singapore has a small multiplier size, k. This is because of its high marginal propensity to save (MPS) due to compulsory savings schemes such as the Central Provident Fund (CPF) where 17% of the monthly income of Singaporeans will be saved. The Asian values of thrift also fostered a diligent saving habit among Singaporeans. Furthermore, Singapore has limited land space for agriculture, thus has to import essentials and foodstuffs, the country also needs to import raw materials and semi finished goods to fuel its export sector. Thus, Singapore also has a high marginal propensity to import (MPM). Since k = 1/MPW, where marginal propensity to withdraw (MPW) = MPS+MPM+MPT, a high MPW will lead to a small k. Hence, since Singapore is already experiencing high demand-pull inflation and is operating at full employment output, a fall in net exports will not lead to a fall in economic growth as the fall in GDP will be a nominal one.

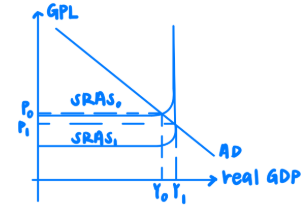

R2: Explain why appreciation to curb imported inflation will not lead to trade-offs with economic growth

Appreciation to curb imported cost-push inflation will not lead to trade-offs. When the SGD is strengthened, imported goods will be relatively cheaper in terms of domestic currency, thus lowering the cost of production of firms due to a decrease in the prices of raw materials. This will lower the unit cost of production of firms, as the same amount of money can be used to acquire more factors of production, thus increasing output. This will cause short-run aggregate supply (SRAS) to increase, shifting it downwards from SRAS0 to SRAS1 while national income increases from Y0 to Y1, thus achieving actual economic growth. Firms will then pass on these cost savings to consumers, resulting in a decrease in the general price level of final goods and services from P0 to P1. The increase in national income will cause output to increase, this unplanned inventory depletion will result in an increase in the derived demand for labour and lowering unemployment. Additionally, a decrease in cost of production will result in firms experiencing an increase in profit levels, assuming that their total revenue remains the same. This will in turn encourage firms to invest more thus further boosting AD and national income, achieving actual economic growth.

Evaluation 2: Might still lead to trade-offs in the economy if the root cause of cost-push inflation is not imported inflation

However, appreciation to curb cost-push inflation might still lead to trade-offs if the root cause of the cost-push inflation is not imported inflation. If the root cause is due to rising wages and utilities expenses, appreciating the SGD will not curb cost-push inflation by making the price of imports cheaper and may even amplify the negative impacts of cost-push inflation by causing AD to fall due to domestic products losing price competitiveness due to a stronger SGD. This might lead to trade-offs with economic growth as the import expenditure outweighs export earnings. Additionally, it also depends on whether Singapore is appreciating against our key importers and not exporters. This is to ensure that Singapore can maintain the prices of imported goods and services low while ensuring its price competitiveness in the foreign market among its key exporters, so as to continue boosting export earnings while keeping cost of production low.

Conclusion

In conclusion, in the Singapore economy, appreciation will more likely not lead to any trade-offs in the economy. This is because of Singapore's small multiplier size, k, which indicates a small fall in AD. while at the same time, Singapore imports make up close to 200% of its real GDP. Hence, the increase in SRAS will outweigh the decrease in LRAS. Additionally, as Singapore is operating at full employment output, appreciation thus leading to a fall in AD may be beneficial to the economy as it will cool off an overheated economy, thus reducing risks of demand-pull inflation. However, in the short-run, reducing inflation through appreciation may still lead to trade-off in terms of worsening the balance of trade as exchange rates require time to be effective due to existing contractual obligations. Thus, a drastic increase in import expenditure will outweigh export earnings in the short run, thus worsening Singapore's balance of trade.