J2: Monetary Policy

NYJC Q3a

The Monetary Authority of Singapore (MAS) has a unique monetary policy framework that focuses on managing the exchange rate rather than interest rates. This approach has implications for the country's macroeconomic objectives.

(a) Explain why Singapore chooses exchange rates rather than interest rates as its main tool of monetary policy.

Introduction

Singapore is a small and open economy with no natural resources, making it highly dependent on imports for essentials and exports for economic growth. As a global financial hub with free capital mobility, Singapore is an interest rate taker and does not rely on interest rate policy like most countries. Instead, MAS manages the economy through exchange rate policy, adopting a modest and gradual appreciation stance of the Singapore Dollar (SGD) to achieve macroeconomic objectives such as price stability and sustainable growth.

R1: Small and Open Economy (Exchange Rate vs Interest Rate policy)

Singapore’s small domestic market (population ~5.7 million) limits the effectiveness of interest rate policy, which primarily affects domestic consumption (C) and investment (I). In most large economies, to stimulate actual growth, central banks typically increase the money supply to lower interest rates, reducing the cost of borrowing. This encourages households to increase spending on big-ticket items (e.g., housing, vehicles), raising consumption (C), while businesses increase investment (I) as previously marginal projects become profitable. The rise in consumption (C) and investment (I) leads to an increase in aggregate demand (AD), boosting national income (NY).

However, in Singapore, the impact of interest rates on aggregate demand (AD) is limited due to its reliance on foreign direct investment (FDI) and its small consumer base. Instead, MAS utilises exchange rate policy, which has a more direct and immediate effect on Singapore’s main driver of growth: net exports (X-M).

For example, when Singapore faces an economic slowdown, MAS may adopt a zero appreciation stance. A stable or weaker SGD makes exports cheaper (Px↓) in foreign currency terms and imports more expensive (Pm↑) domestically. Assuming the Marshall-Lerner Condition (MLC) holds, export revenue increases and import expensive falls, increasing aggregate demand (AD) and National Income (NY).

Given Singapore’s trade-to-GDP ratio exceeding 300%, the exchange rate has a more significant influence on national output compared to adjustments in consumption (C) and investment (I).

R2: Nature of Inflation

Unlike interest rate policy, which mainly influences domestic demand—consumption (C) and investment (I)—to manage only demand-pull inflation, Singapore’s exchange rate policy is more versatile, effectively tackling both demand-pull and imported cost-push inflation simultaneously. This makes exchange rate management a more suitable monetary policy tool for Singapore, given its economic context.

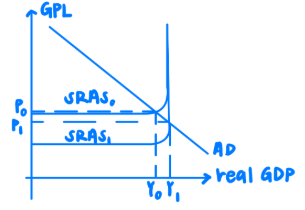

Singapore is particularly vulnerable to imported cost-push inflation because of its heavy reliance on imports for essentials such as food, energy, and raw materials given the lack of natural resources. By adopting an appreciation stance, MAS strengthens the SGD relative to foreign currencies, reducing the domestic currency price of imported inputs. This lowers production costs for firms, shifting the short-run aggregate supply (SRAS) curve rightward from SRAS0 to SRAS1, thus reducing cost-push inflation and lowering the general price level from P0 to P1.

Additionally, Singapore frequently operates near its full employment output level, with the unemployment rate standing at 1.9%, below the natural rate of unemployment. This places the economy at risk of demand-pull inflation. An appreciation makes Singapore’s exports more expensive in foreign currency terms and imports cheaper domestically, reducing net exports (X-M). Assuming Singapore’s exports are price elastic, the appreciation leads to a more than proportionate fall in export demand and a rise in import spending. This causes AD to fall, reducing inflationary pressures and helping to prevent overheating in the economy. Thus, the ability of exchange rate policy to manage both forms of inflation simultaneously aligns closely with Singapore’s macroeconomic objectives, further explaining MAS’s choice of exchange rate management over interest rate policy.

R3: Free Capital Mobility and the Trilemma Constraint

Singapore does not use interest rate policy due to the macroeconomic trilemma. As a global financial hub, Singapore allows free capital mobility to attract investment and maintain financial credibility. Under the trilemma, a country cannot simultaneously maintain a managed exchange rate, free capital flows, and an independent interest rate policy. Singapore prioritises managing the exchange rate through a trade-weighted basket (S$NEER) to ensure price stability and export competitiveness.

If MAS were to raise domestic interest rates, Singapore’s interest rate would become relatively more attractive than that of other countries, leading to capital inflows (hot money) from global investors seeking higher returns. The resultant increase in demand for SGD would exert upward pressure on the exchange rate, causing it to appreciate sharply.

This appreciation introduces exchange rate volatility, which is undesirable for a trade-reliant economy like Singapore. Volatile exchange rates affect both export competitiveness and the predictability of import costs, creating uncertainty for businesses and potentially heightening inflation volatility. As such, MAS avoids using interest rate policy and instead relies exclusively on exchange rate management to achieve price stability. As such, given this constraint, Singapore is effectively an interest rate taker, with domestic interest rates determined by global financial conditions rather than local policy choices.

Conclusion

In conclusion, Singapore’s status as a small and open economy, its vulnerability to both cost-push and demand-pull inflation, and the limitations posed by free capital mobility explain why MAS uses exchange rate policy—specifically a modest and gradual appreciation stance—as its primary monetary tool over interest rate policy.