J2s: Fiscal Policy (pt2)

YIJC 2024 prelims Q5

In 2022, Singapore’s economy was impacted by global events such as the ongoing supply chain disruptions caused by the Russia-Ukraine war, which led to increased energy prices and inflation. Additionally, the tightening of global monetary policies by major economies, including the Federal Reserve’s interest rate hikes, put further pressure on Singapore’s export-driven economy.

b) Discuss the policies implemented by the Singapore government to mitigate the adverse consequences brought by the above global events.

Introduction

As mentioned in the preamble, “ongoing supply chain disruptions” and “the tightening of global monetary policies by major economies” can adversely affect Singapore’s economy. These global events typically lead to imported cost-push inflation due to higher import prices, falling export earnings due to lower national income in trading partners, and rising unemployment from falling output. In response, the Singapore government has implemented policies such as the exchange rate policy and expansionary fiscal policy. This essay assesses how each policy works, their limitations, and their effectiveness in addressing these external shocks.

R1: Exchange rate policy - to solve supply chain disruptions that cause high energy prices and inflation

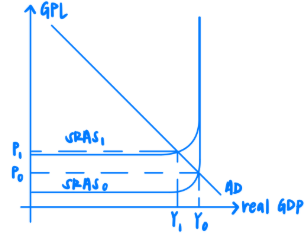

One key adverse consequence mentioned in the preamble is the rise in energy prices and inflation due to ongoing supply chain disruptions from the Russia–Ukraine War. As Singapore is highly reliant on imports for food, energy, and intermediate goods, higher global prices raise domestic production costs, resulting in imported cost-push inflation. This shifts the Short-Run Aggregate Supply (SRAS) leftward from SRAS₀ to SRAS₁, leading to a fall in real national income from Y₀ to Y₁, slowing economic growth and raising unemployment as labour is a derived demand.

A modest and gradual appreciation of the Singapore Dollar (SGD) helps mitigate this by reducing the domestic currency price of imports (fall in Pm). With lower imported input costs, firms face reduced production expenses, shifting SRAS back rightward from SRAS₁ to SRAS₀. The general price level falls from P₀ to P₁, curbing imported cost-push inflation. At the same time, the recovery in SRAS leads to a rise in real output, increasing national income from Y₁ back to Y₀, achieving actual and hence economic growth and lower unemployment. Thus, appreciation not only maintains price stability but also helps reverse the decline in actual growth caused by earlier supply-side disruptions.

Evaluation 1: Limitations of exchange rate policy

While appreciation helps reduce imported cost-push inflation, it also causes Singapore’s exports to become more expensive in foreign currency terms (rise in Px), reducing export price competitiveness. At the same time, it makes imports cheaper in SGD terms (fall in Pm), encouraging both consumers and firms to switch towards foreign goods. Assuming the Marshall-Lerner Condition holds (PEDx + PEDm > 1), the more than proportionate fall in quantity demanded for exports and the more than proportionate rise in quantity demanded for imports leads to a fall in export revenue (X) and an increase in import expenditure (M). As a result, net exports (X – M) fall, worsening the balance of trade (BOT), which is a component of the current account.

That said, Singapore’s exports—such as pharmaceuticals and semiconductors—tend to be high-value, skill-intensive goods with few close substitutes. These exports are largely non-price competitive and thus relatively price inelastic. As a result, the fall in quantity demanded may be less than proportionate, and export revenue (X) may only fall slightly. While the BOT may deteriorate slightly, Singapore’s persistent current account surplus is likely to be maintained.

R2: Expansionary fiscal policy to solve fall in economic growth

Another key adverse consequence brought about by the Federal Reserve's interest rate hike is a sharp fall in Singapore’s economic growth. Singapore is an interest rate taker, thus when interest rates are raised, households are discouraged to purchase big-ticket items as the opportunity cost to spend increases. Firms will also be discouraged from investing as lesser projects are profitable. Consumption (C) and investment expenditure (I) will both fall, thus leading to a fall in AD and national income.

OR

The Federal Reserve’s interest rate hike indicates an increase in cost of borrowing in the US. This discourages households and firms to purchase big-ticket items and increase investment expenditure respectively as the opportunity cost to spend increases while more projects become unprofitable. As the C and I of USA falls, their AD falls, leading to a subsequent decrease in national income. Given that USA is a close trading partner of Singapore, a fall in their national income will lead to a fall in purchasing power and hence a fall in demand for Singapore’s exports. This will thus lead to a fall in Singapore’s export earnings (X), AD, and national income.

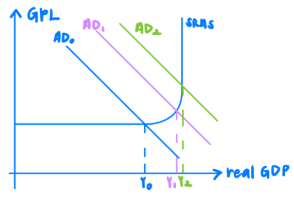

To address this, the government can implement expansionary fiscal policy through increased government spending (G) or tax reductions (T). As G is a component of AD, higher public expenditure on infrastructure, wage support, or digital initiatives directly raises AD. Simultaneously, a cut in personal income taxes raises household disposable income (Yd), boosting consumption (C), while a cut in corporate taxes improves firms’ after-tax profits, encouraging investment (I) as more projects become viable.

As government spending (G), consumption (C), or investment (I) increases, aggregate demand (AD) rises, leading to a rise in national income (Y). With higher income, households experience an increase in disposable income and respond by increasing their consumption. This rise in induced consumption causes a further increase in AD and generates a second-round rise in national income. However, in each successive round, a portion of the additional income is withdrawn from the circular flow through savings, taxes, and imports. As a result, the increase in spending becomes smaller in each round until it becomes negligible. Through this positive multiplier process, national income increases by a multiple of the initial injection. AD shifts rightward from AD₁ to AD₂, increasing real output from Y₁ to YF, spurring economic growth and reducing unemployment as labour is a derived demand.

Evaluation 2: limitations of expansionary fiscal policy

While expansionary fiscal policy can be effective in addressing a fall in aggregate demand, it often requires the government to run budget deficits, especially when implementing large-scale subsidies, infrastructure projects, or tax cuts. These deficits must be financed through either borrowing or drawing down on Singapore’s national reserves. Both financing methods create long-term fiscal implications.

Borrowing raises the national debt, which will require future repayment with interest, placing a financial burden on future budgets. This may force the government to raise future taxes or reduce essential public spending. Drawing down reserves, while feasible for Singapore, reduces the buffer available to respond to future economic shocks. Over time, both approaches can result in reduced fiscal space for long-term investments such as education, infrastructure, or healthcare—key drivers of sustainable economic growth.

OR

The effectiveness of fiscal policy depends on the size of the multiplier, given by the formula k = 1 / (MPS + MPM + MPM). In the case of Singapore, the multiplier tends to be small due to both cultural and structural reasons. Singaporeans have a high marginal propensity to save (MPS), influenced by Asian values of thrift and the CPF system, which is a mandatory savings plan where individuals are to save 37% of their income into CPF (20% employee, 17% employer). At the same time, Singapore has a high marginal propensity to import (MPM) as a small, open economy with no natural resources, and hence relies heavily on imported goods and services. These leakages reduce the portion of additional income that is spent domestically in each round of the multiplier process, limiting the overall impact of fiscal policy on national income.

Final evaluation + conclusion

In conclusion, while modest and gradual appreciation of the SGD can address imported cost-push inflation, it may lead to a fall in net exports and aggregate demand. Fiscal policy can mitigate pessimism-induced falls in demand and unemployment, while FTAs serve as a long-term strategy to strengthen supply resilience and price stability. However, no single policy is universally optimal.

The effectiveness of each policy depends on the specific root cause of the economic challenge. For instance, appreciation is best suited for tackling inflation driven by higher import prices, whereas fiscal policy is more appropriate for addressing weak domestic demand and unemployment. FTAs are effective for enhancing long-term resilience but are not suitable for immediate stabilisation. This is because signing and implementing FTAs is a time-consuming process that requires mutual trust, sustained diplomacy, and strategic alignment between nations. For example, Singapore’s extensive FTA network took decades of active bilateral and multilateral engagement to build.

Hence, the Singapore government should use a mix of policies both in the short run and long run to effectively target the negative effects derived from external shocks, implementing both immediate and long-run policies to complement each other and maximise the benefits of these measures while minimising the constraints.